Reindustrialisation

Reindustrialisation 4.0 - what is the path to the future for the industrial sector?

The digital revolution and the need to combat climate change, together with the recent COVID-19 pandemic, but above all, have put the reindustrialisation debate on the table. A new type of industrialisation that, rather than using out-dated models, is based on ones that back digitalisation and sustainability.

Relocation of production, the 2008 financial crisis and the coronavirus pandemic have weakened the industrial sector over the last 20 years, principally in the West. Due to this situation, and the threats inherent in climate change, many governments are backing a green and digital reindustrialisation — also called reindustrialisation 4.0 — to revive the sector.

The present-day industrial sector

The COVID-19 pandemic has also had a huge impact on the industrial sector. According to a 2020 report from the United Nations Conference on Trade and Development (UNCTAD), the drop in production in China, a country on which many industrial sectors depend for the supply of intermediary inputs, will bring about a $50bn drop in global supply chains.

The most severely affected area, according to this UNCTAD report, will be the European Union (EU) with losses of $15.6bn, followed by the USA with $5.8bn. The most heavily-hit sectors include chemicals (-129 million) and textiles (-64 million), although others will also be affected such as automobile, metallurgy and industrial machinery.

A new industrial model: reindustrialisation 4.0

Right now, many governments are launching reindustrialisation programmes to help the sector to recover muscle, by increasing its weight in the economy and strengthening its resilience. An example of this is the initiatives undertaken by the US in this direction in recent years:

- In 2014, the EU produced a road map for the reindustrialisation of the zone with the publication of the report Towards a European Industrial Renaissance

External link, opens in new window.. This document stated that "a strong industrial base is fundamental for European competitiveness and recovery" and a target was set: for the industrial sector to represent 20 % of its GDP by 2020 - compared to 15.1 % for 2013. To achieve this, attention was drawn to the need to have an integrated infrastructure comprising transport, information and energy networks.

External link, opens in new window.. This document stated that "a strong industrial base is fundamental for European competitiveness and recovery" and a target was set: for the industrial sector to represent 20 % of its GDP by 2020 - compared to 15.1 % for 2013. To achieve this, attention was drawn to the need to have an integrated infrastructure comprising transport, information and energy networks. - In 2016, the EU decided to develop this approach through the so-called Industry 4.0 strategy. Going one step further, the European Commission urged industry to take advantage of the technological innovations arising from the digital revolution, such as the Internet of Things (IoT), robotisation and artificial intelligence, machine learning, big data and 5G in a comprehensive and sustainable way, considering it to be "an essential requisite in order to ensure the competitiveness of Europe in the medium and long term with implications for general well-being".

This route map from the EU with regard to reindustrialisation, together with the European Green Deal reflect the double transition — sustainable and digital — which pave the way towards the future not only of the industrial sector in Europe, but also for the economy and society as a whole throughout the world. In the US, for example, the president, Joe Biden has declared his intention to reindustrialise numerous sectors to move towards clean energy — a plan which he promises will create up to 10 million jobs. In this way the North American giant hopes to level the scales against the rise of countries like China and India. This is a route which, following COVID-19 and despite the existence of discordant voices, is also being considered by countries such as Brazil, Russia, Australia or South Africa.

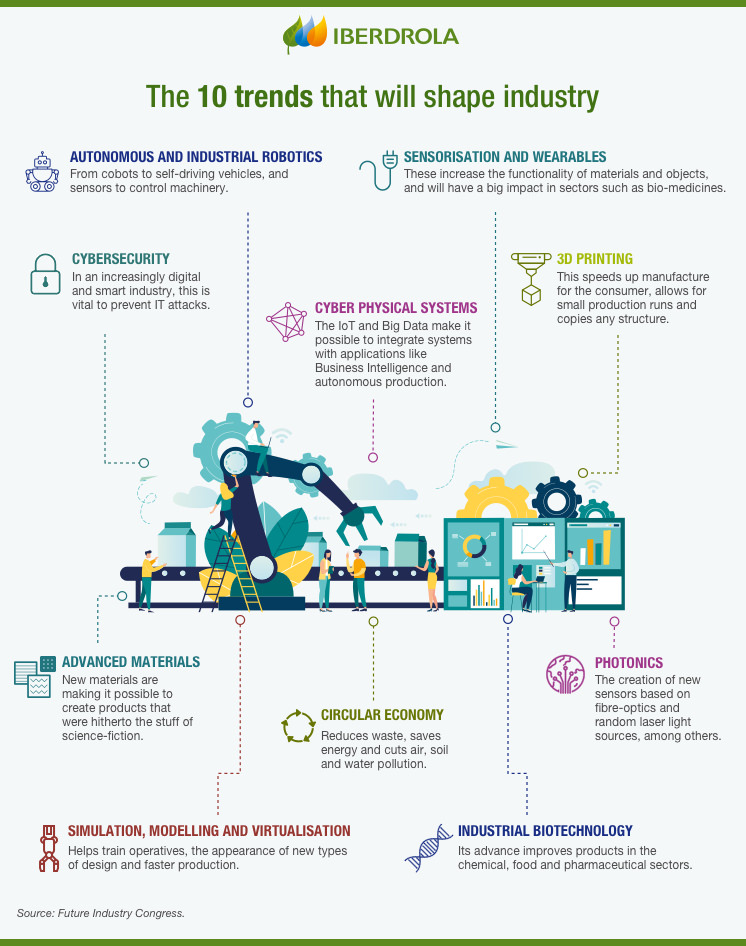

The keys to reindustrialisation 4.0

The future of industry largely embraces the following concepts: innovation, digitalisation, and sustainability. Let's look at how each of those concepts impacts on the sector:

Sustainable industry

Sustainable industry

Given the current crisis brought about by the coronavirus and the threats inherent to climate change, many multilateral organisations, governments and leading members of the business and financial sectors are highlighting the need for a Green Recovery that can revive the economy and employment at the same time as increasing resilience to future systemic shocks. This means both combating climate change through decarbonisation — with the ensuing boost for renewable energy — and embarking on a transition from a linear economy to a circular one.

Digital industry

Digital industry

The digital revolution is transforming industry, opening the door for new models of production and smart factories capable of using the same resources to produce more and higher quality products tailored to the needs of customers, at the same time as cutting emissions, energy consumption and waste. Similarly, digital technologies are also supporting the emergence of new business opportunities such as eHealth, smart farming and digital profiles linked to industry.

Innovative industry

Innovative industry

In a world in which the boundaries between the physical and digital worlds are becoming increasingly blurred, the dominance of technologies and the ability to introduce disruptive innovations will be decisive to market positioning. And we are no longer just talking about companies investing more and more in R+D+i, but about the fact that the reindustrialisation of each country or economic area means joint investments at the sectoral level, involving universities and public authorities so as not to lose market share over other areas.

How to define a reindustrialisation strategy

According to consultants Deloitte, a reindustrialisation strategy should answer four basic questions: what is the objective, where are we competing, how to win and what is needed to execute the defined strategy. Focusing on these questions, five challenges can be formulated:

- Positioning. Choosing which industrial sub-sectors to compete in. This means having detailed knowledge regarding both the national and foreign industrial fabric.

- Focus. Defining those activities within each industry in which national companies can develop a sustainable competitive advantage.

- Size. In the medium term, it will become necessary to overcome the structural limitations of SMEs and grow in order to compete in an international context.

- Talent. On the one hand, improving national talent productivity through training, and on the other, attracting foreign talent.

- Operational R+D. Maximising the efficiency of the capacity to spend on R+D by national companies, overcoming limitations associates to size.

Circular economy model at the Iberdrola Group

At Iberdrola, we are working to be more respectful of nature through our three strategic sustainability priorities: climate action, biodiversity protection and the circular economy.

For this reason, our sustainable business model is based on circular economy principles, a resource-management system that prioritises reducing the use of new raw materials through process efficiency, extending product life cycles and promoting the reuse and recycling of materials.

We apply this approach throughout our value chain, building a decarbonised future alongside strategic partners who share our vision and values for environmental protection and preservation.

In 2025, we carried out circular economy initiatives related to wind turbine blade recycling, radioactive waste storage and reducing gas consumption.